Banking Contagion Is Closer Than You Think

What’s Happening Now—and What Comes Next

You haven’t seen the headlines yet, but they’re coming.

Right now, something’s breaking in Japan’s financial system. Norinchukin Bank—one of the country’s largest—just posted over $12 billion in losses after dumping bonds that no longer made sense to hold. Their central bank is reversing course, injecting liquidity back into the system. The yen is dropping. And people are starting to notice.

It’s quiet, but it won’t stay that way. Because this isn’t just Japan’s problem.

When a system is as tightly connected as global finance, small cracks don’t stay small. They spread. And if we’re right, what starts in Japan will flow through Europe and eventually hit the U.S.—dragging markets, banks, and small businesses along for the ride.

What follows is my best guess at how it unfolds from here. The sequence feels clear. The signs are everywhere. But let’s be honest—timing is always the hard part. Seeing the writing on the wall is easy. Calling the moment it tips is something else entirely. So treat the timeline as a framework, not a forecast. The signal matters more than the schedule.

Let’s walk through what’s unfolding, what could come next, and what it all means for those of us paying attention.

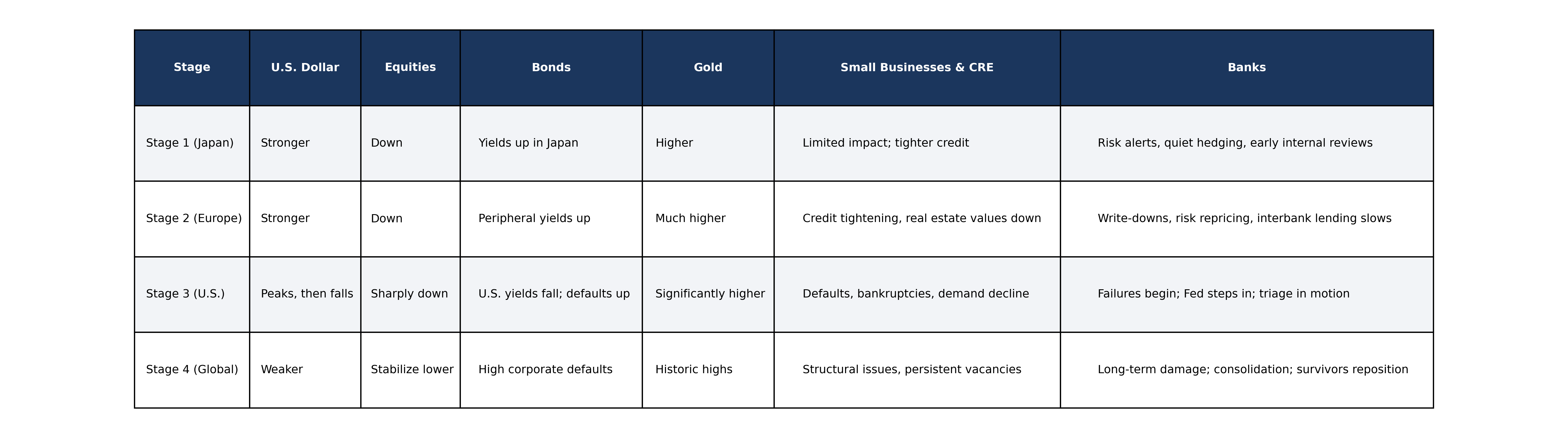

Stage One: Japan’s Breaking Point

Estimated Timeline: June–August 2025

Japan has been managing its financial system like a Jenga tower for decades—carefully, deliberately, and with a fair amount of quiet panic. The Bank of Japan held rates near zero, propped up bond markets, and tried to keep everything balanced. Until they couldn’t.

Norinchukin’s losses were the first public sign that the game was over. The BOJ, sensing real trouble, paused rate hikes and quietly restarted its money-printing machine. The yen slipped hard. Bond yields jumped. And investors ran for the exits.

Here’s what changes:

The yen weakens sharply.

Japan’s stock market takes a hit.

Global bond markets start to feel pressure as Japan dumps Treasuries to raise cash.

Gold ticks upward as the early warning crowd starts moving.

What it means for small business:

Not much right away. But lenders start to get a little twitchy. Credit conditions tighten just a hair. And if you rely on imported goods, that weakening yen could start to matter.

What it means for banks:

The radar lights up. Risk teams start modeling exposures. Trading desks quietly trim positions in Japanese debt. Nobody’s panicking, but internal memos are flying. A few banks start rethinking hedges. The smartest ones are already calling meetings.

This is the spark. The next stage is where things start to spread.

Stage Two: Europe Feels It Next

Estimated Timeline: September–November 2025

Big European banks are tangled up in Japan in all kinds of ways—through bond exposure, structured products, and complex derivatives. When Japan sneezes, Europe catches the flu.

As losses mount, the usual suspects—Deutsche Bank, some French and Italian players—start showing signs of stress. Bond yields in southern Europe spike. The ECB scrambles to calm things down. But confidence is fragile, and the timing couldn’t be worse.

What changes:

European banks start reporting hits tied to Japan.

Sovereign debt in places like Italy and Spain starts looking risky again.

European stocks take a dive.

The euro weakens, and the dollar gets stronger—again.

What it means for small business:

Credit gets tighter. Lenders start asking more questions. Deals take longer. In Europe, real estate prices start to soften. In the U.S., the equity markets wobble harder. Still no full-blown crisis—but it feels a lot less like background noise now.

What it means for banks:

Losses go from theoretical to real. Interbank lending slows. Derivative counterparty risk gets repriced. A few institutions get downgraded. Risk officers start earning their paychecks. The U.S. banking system isn’t hit directly yet—but everyone’s watching what’s on their books.

Stage Three: The U.S. Takes a Hit

Estimated Timeline: December 2025–March 2026

At first, the U.S. looks like a safe haven. But that doesn’t last. Exposure to Japanese and European assets starts showing up on the balance sheets of big American banks. Regional banks—already exposed to commercial real estate—start to struggle.

The Fed steps in, just like they always do. Rates come down. QE ramps up. But inflation’s still hanging around, and that makes everything harder.

What changes:

Big banks take write-downs. Regional banks fail.

CRE defaults pick up, and vacancies rise fast.

The stock market takes a real hit—major indices down 20–30%.

Gold surges. People want something that doesn’t move with the Fed.

What it means for small business:

This is where it starts to hurt. Access to capital dries up. Loan covenants get stricter. CRE owners can’t refinance. Layoffs begin. Customers pull back. And if you’re not ready, it gets ugly fast.

What it means for banks:

The pressure gets real. CRE portfolios crack. Borrower defaults accelerate. Deposits start to flow—first to the big banks, then into cash and gold. Regional banks scramble for stability. The Fed opens emergency funding windows. Nobody wants to admit it, but we’re back in triage mode.

Stage Four: The Aftershocks

Estimated Timeline: April–June 2026

By now, the financial side of the crisis is clearer. The political side starts to show up.

There’s outrage. There’s blame. There’s talk of new taxes, bailouts, investigations. Populism rises across the political spectrum. And as always, the idea of “foreign distractions” starts to get louder. Tariffs, tensions, troop movements—anything to change the subject.

What changes:

The dollar weakens. People are watching the Fed—and losing patience.

Stocks settle at lower valuations. Defense and energy names start to lead.

Corporate debt markets stay shaky. High-yield defaults climb.

Gold hits historic highs.

What it means for small business:

Some companies make it through. Others don’t. A lot of people leave the workforce. Real estate deals stall. Vacancies stick around. Margins shrink. Demand stays soft. This is the long tail of a slow-moving crisis.

What it means for banks:

The damage is done—and now it’s about recovery. Balance sheets are bruised. Lending appetite is down. Regulatory pressure picks up. M&A talks start. Some banks go quiet. Others go hunting. The ones who led early? They’re in the best position to rebuild.

A Quick Look at the Trendline

If You’re a Small Business Owner…

Let’s be blunt: this won’t hit everyone the same way. But the trend is clear.

You need to think about:

Cash flow: Stop assuming it’ll be stable.

Debt: Refinance while you still can.

Demand: Budget for less, not more.

Growth: Focus on surviving first.

You don’t have to panic—but you do need to prepare. And if you wait until things are obvious, you’ll be too late.

And If You’re a Banker?

It’s time to ask one simple question: Is your SBA partner paying attention?

Because if your CDC isn’t talking about these shifts—if they’re not watching Japan, or Europe, or the real estate market—then they’re just reacting. And in times like these, reacting isn’t enough.

This is what sets us apart.

At B:Side, we believe it’s our job to look up and out—not just down and in. We analyze. We anticipate. We speak up when others stay quiet. And we don’t wait for the crisis to hit the front page to start planning for it.

That’s how we help our banking partners stay a step ahead. And in a year like this, that edge matters.

One Last Thing

Last week, I wrote that saving the bond market might mean sacrificing stocks. That wasn’t a prediction—it was an observation. A sign that the ground was already shifting.

This week, I’m saying the cracks are spreading. Japan is the starting point. Europe’s the middle. The U.S. is the destination.

It won’t all happen at once. But it is happening.

You can ignore it, or you can prepare. You can wait to be told what it means, or you can work with people who already know.

Look up. Look out. Stay ahead.