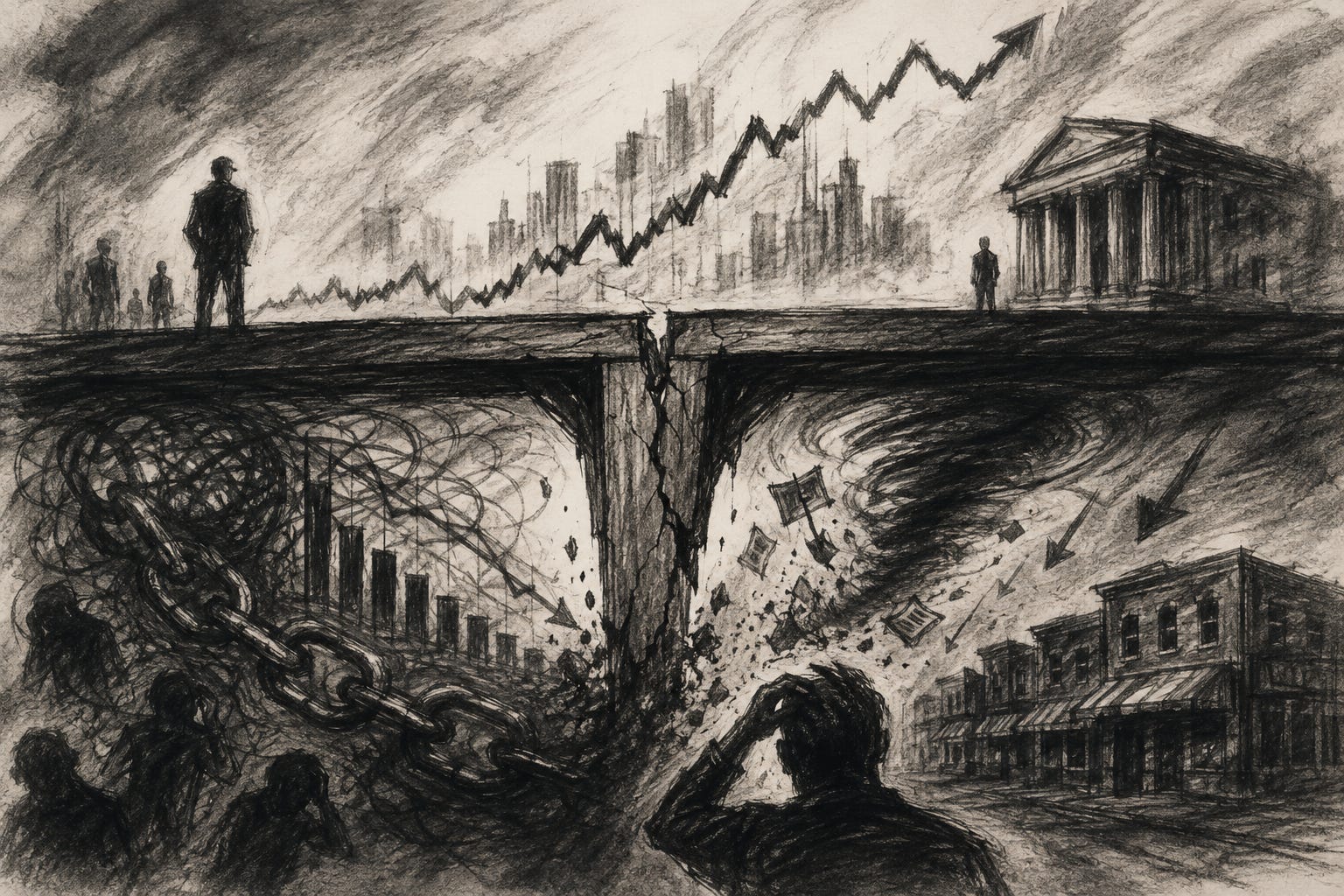

The Load-Bearing Market

In a system built on borrowed money, the price level does structural work. When it falls far enough, the credit it holds up falls with it.

Lately I keep getting versions of the same question from team members, students, and readers alike. While they come from different backgrounds and perspectives, they share one thing in common: they can’t shake a particular unease. It runs something like this: why does nothing seem to touch the market anymore?

Whatever happens, the market shrugs it off and grinds higher. A war in one region, a debt downgrade, a hot inflation print, a political crisis that would have rattled an earlier generation of investors. Each one hits, the screen wobbles for a day, and then the momentum reasserts itself and prices push to new records. The optimism feels almost untethered. And it runs directly against what many of us are actually seeing. In our small business portfolio, the strain is real and getting harder to miss: thinner margins, slower payments, a smaller buffer than there was a year ago. A lot of the people I talk to carry the same quiet dissonance in their own lives, a sense that the numbers on the screen and the conditions on the ground have come apart.

So the question sharpens into something more pointed. Why are the powers that be so willing to pull out every stop, to go to any length, no matter how unprecedented the move, to keep the market from falling?

The answer is the uncomfortable one. They have no other choice.

To understand why, you have to set aside the way most of us instinctively think about the stock market. We treat it like a thermometer, a reading of how the economy is doing. The number goes up and we feel good about where things are headed; the number goes down and we worry. But the people who actually run the financial system know something the thermometer framing hides. The market does two jobs at once. It measures the economy, and it helps hold the economy up.

That second job is the one almost nobody talks about, and it is the reason a falling market is so much more dangerous than a falling thermometer. A thermometer that drops only tells you it is cold. A price that drops, in a world this leveraged, makes it colder.

The Market Looks Calm. That Is the Setup.

Right now the conditions look benign. The S&P 500 is sitting just under its record high, less than a percent off the top. The VIX, the market’s fear gauge, is down around 16, near the sleepy end of its range, even though it touched 35 within the past year. Volatility is low. Confidence is high.

That calm is not the opposite of risk. It is how risk gets built. Hyman Minsky spent his career on this single idea, and it is worth saying plainly: stability is destabilizing. When times are good for long enough, borrowers and lenders both relax. Loans that once looked prudent start to look timid. Leverage that once felt aggressive starts to feel normal. The longer the calm holds, the more debt the system piles on top of it, until the whole structure quietly depends on the calm continuing.

You can see the pile in the numbers. Investor margin debt, the money people borrow against their portfolios to buy still more, hit a record in April: $1.3 trillion, up more than fifty percent in a single year. As a share of the economy, analysts put it at an all-time high, well past where it stood at the dot-com peak in 2000. The borrowing did not climb in a smooth line, either. It dipped earlier in the year and then jumped by more than $80 billion in one month to set the record. That is not the behavior of patient money. That is the procyclical reflex the leverage literature has described for decades: people borrow more precisely when prices are high and the mood is good, which is exactly when they should be doing the opposite.

A Price Drop Is a Credit Event

To see why a drop is so dangerous, you have to understand what collateral actually does in a modern financial system.

When you borrow against an asset, the lender protects itself by lending a little less than the asset is worth. The gap is the haircut, the cushion. As long as the asset holds its value, everyone is fine. But the moment the price falls, two things happen at once. The borrower’s equity shrinks, and the collateral backing the loan is suddenly worth less than it was. The lender, doing nothing wrong and following its own rules, asks for more: more cash, more collateral, a bigger cushion. The borrower can raise that cash quickly in only one way. By selling.

Here is the part that turns a correction into a crisis. When enough borrowers are forced to sell at the same time, their selling pushes prices down further. Lower prices mean lower collateral values, which trigger more calls, which force more selling. The loop feeds itself. Economists have given the two halves of this loop precise names. There is the loss spiral, where falling prices wipe out the equity of leveraged holders and force them to dump assets, and the margin spiral, where the same falling prices and rising fear lead lenders to demand fatter cushions at the worst possible moment. Brunnermeier and Pedersen showed that the two spirals reinforce each other, and that the combined damage is larger than the sum of the two.

Underneath it all sits Irving Fisher’s cruel arithmetic from 1933. When everyone deleverages at once, selling assets and paying down debt together, they drive prices down so fast that the real weight of the remaining debt actually rises. In his phrase, the more the debtors pay, the more they owe. Trying to climb out of the hole collectively digs it deeper.

This is the insight the thermometer framing misses. In a collateralized system, the price level helps determine how much credit can exist at all. Collateral value sets borrowing capacity. So when prices fall, the system’s capacity to lend contracts on its own, by mechanics rather than mood. The drop in price is the drop in credit.

The Leverage Has Moved

The margin-debt record is the figure that makes headlines, because it is visible and it is retail and it is easy to picture: ordinary investors borrowing against their stocks. But if you are looking for where the next spiral actually starts, that regulated retail number is no longer where the real danger sits.

The bigger and faster risk has migrated into the plumbing, into the part of finance that does not have a ticker. Hedge funds have built enormous positions in the Treasury market, the supposedly safest market in the world. Their long Treasury exposure has grown from roughly $600 billion a decade ago to about $2.4 trillion at the end of last year. They fund much of it through repo, short-term borrowing against those same Treasuries, and their net repo borrowing has reached around $1.8 trillion, more than double what it was at the start of 2024. The Federal Reserve describes this leverage as near all-time highs, concentrated in a small number of very large funds.

Here is the detail that should make you sit up. Much of that borrowing is done at zero haircut. No cushion at all. In 1929, the speculative fuel was the call loan: investors buying stocks with as little as ten percent down. We look back at that leverage as reckless. The modern version is larger, it sits inside the Treasury market rather than the stock market, and in places it runs with no cushion whatsoever. It is the same machine, bigger and better hidden.

And this is only one room in a very large house. The non-bank financial system, the hedge funds and private credit funds and money market funds and all the rest, has grown to roughly $257 trillion globally. It is now larger than the traditional banking system. Leverage behaves like water. After 2008, regulators built strong walls around the banks, so the leverage flowed downhill to the places where the walls were lowest. That is where it pooled.

Safer in the Banks, More Fragile in the Shadows

Now, I know what some of you are thinking. Haven’t we been through all this? We rebuilt the system after 2008. Banks hold far more capital than they used to. They get stress-tested every year against brutal scenarios. The Fed has a standing facility that can pump cash into the repo market on demand. All of that is true, and none of it should be waved away.

But the honest answer to “is it different now?” is unsettling. We are safer in the banks and more fragile in the shadows. The reforms did their job at the core. Large banks carry capital near historic highs and would survive losses that would have killed them two decades ago. What the reforms did not do, could not do, was stop the leverage from moving. It moved to the funds and the markets where supervision is thinnest, and where a spiral can run before anyone with authority can see it clearly.

There is a backstop coming. New rules will push much of the bilateral Treasury market into central clearing, with real margin and a mutualized structure behind it. It is a genuine improvement. It is also not live yet. The cash-clearing piece is not scheduled to begin until the very end of this year, and the repo piece not until the middle of next. The protection we are counting on is still months away. The exposure is here now.

The Spiral Doesn’t Stay on Wall Street

It would be easy to read all of this as a Wall Street story, a problem for hedge funds and the people paid to regulate them. Watching credit conditions for a living, I think that is the most dangerous misread of all.

When a deleveraging spiral runs, it does not stay contained. The first channel is the wealth effect in reverse. Stock ownership in this country is extraordinarily concentrated: the top ten percent of households own roughly eighty-seven percent of all stocks. When the market falls hard, it hits exactly the households that drive the bulk of discretionary spending and investment, and they pull back. A market event becomes a spending event.

The second channel is the one I watch most closely. As collateral values fall and risk rises, lenders retreat. They tighten standards, shrink credit lines, and back away from anything that looks uncertain. And the lending that dries up first is rarely to the largest, safest borrowers. It is to small businesses, the Main Street borrowers who have the least collateral and the smallest margin for error. They feel a Wall Street spiral as a closed door at the bank, often before the headlines have caught up to what is happening. The banks themselves are now lending heavily into those non-bank funds, which means stress in the shadows flows right back onto bank balance sheets, and from there into the real economy that the rest of us live in.

This is why the speed of a drop matters as much as its size. A market can fall ten percent in a matter of days now, and modern tools compress those moves further. The counter-forces, the bargain hunters and the policymakers, both need time to act. A spiral does not give them time. The clearest recent warning is Britain in the autumn of 2022, when a sudden jump in government bond yields forced pension funds to sell those same bonds to meet collateral calls, which drove yields higher, which forced more selling. That loop ran in hours, not weeks. Only an emergency central bank intervention stopped it. Most market falls do not become spirals. The ones that do, though, can run faster than judgment can keep up.

What You Do Before the Floor Moves

Let me be clear about what this piece is and what it isn’t. This is not a market call. I am not telling you to sell, or to predict the timing of something no one can time. The whole point of a spiral is that it is unpredictable in its trigger and merciless in its mechanics. What you can do is decide, in advance, which side of it you want to be on. Because every one of these episodes, from 1929 to 2008 to 2020, comes down to the same brutal sorting: the forced sellers lose, and the people with cash and patience buy what the forced sellers have to dump.

So the work is to make sure you are never the forced seller.

For anyone leading a business, that means treating your own leverage as a deliberate choice rather than something you back into. Borrow for things that produce durable cash flow, not for things that only work if prices keep rising. Hold more liquidity than feels efficient in good times, because the entire value of that liquidity reveals itself in the moment everyone else is scrambling for it. Taleb’s framing is the right one here: in a fragile system you want optionality, the capacity to act when others can’t, rather than the brittle efficiency that looks brilliant right up until it shatters.

For the small business owners and the lenders who serve them, the message is more specific and more urgent. Secure your credit before you need it. A line of credit you arrange in calm conditions is a very different thing from one you go looking for in a panic, when the same spiral hammering Wall Street has quietly convinced your bank to stop saying yes. Credit availability does not fade gently in a crisis. It vanishes at exactly the moment you reach for it. The businesses that come through these periods are usually the ones that built their buffer while they still could, while it still felt unnecessary.

What the Number Actually Is

When you hear a policymaker or an executive talk the market up in a tense moment, it is tempting to dismiss it as cheerleading, or vanity, or spin. Sometimes it is. But underneath the spin is a hard structural truth they understand better than most. In a system this leveraged, the price level is load-bearing. The number on the front of the building tells you what the building is worth. It is also one of the beams holding the building up.

A market that falls and then recovers quickly reseats the beam, and the structure holds. A market that falls and stays down long enough lets the spiral do its work, pulling the beam out one stress at a time. That is the difference between a correction and a crisis, and it is far thinner than most people assume.

None of this is a reason to live in fear of a number on a screen. It is a reason to understand what the number actually is. The students I teach will spend their careers being told the market is a scoreboard, a measure of how well things are going. The truth is heavier than that, and more useful to carry. The market is part of the structure now. And the first job of anyone responsible for anything, a portfolio, a company, a payroll, is to make sure that when the structure shakes, you are standing on something of your own.

The market is one place where change can arrive suddenly and violently, but it is hardly the only one. The same is true of the pressures that test a leader. My book, Honor Under Pressure, is about cultivating your leadership code before that pressure hits, because in an era when the ground can shift in hours rather than years, character is the one thing that has to be built in advance. You can find it at www.thefourthturningleader.com.